White paper

Multi-partitioned kdb+ databases:

an equity options case study¶

Kdb+ is well suited to managing massive datasets and offers an unrivalled performance advantage when it comes to processing and analyzing data. This is a case study highlighting some of the key points we have found with regard to the storage and maintenance of financial equity options data in kdb+. We also provide some examples of possible ways to design and query these large databases efficiently.

Overview of the dataset¶

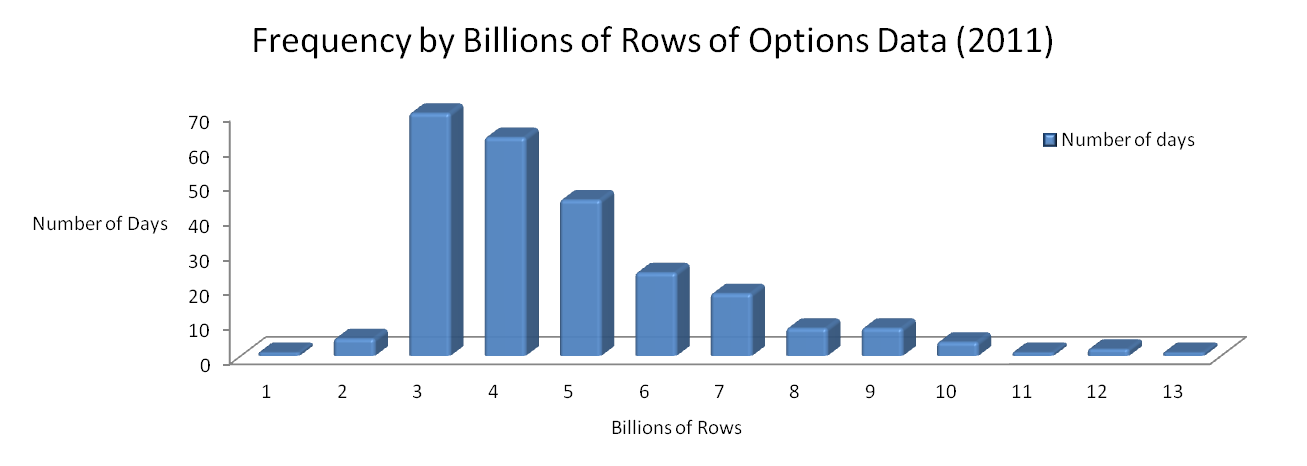

The equity-options data universe is one of the largest financial datasets generated, and more often than not the most challenging dataset for trading firms to manage and extract value from in a timely manner. Hundreds of gigabytes of trade and quote records are published daily from the equity options feeds, with recent daily row count volumes for Q1 of 2012 having an average and maximum count close to 4 billion and 6 billion rows respectively. These numbers represent a relief of sorts from the peaks of 2011 where we saw a maximum daily row count of over 13 billion as highlighted in the chart below.

The dataset we use for our examples in this paper includes level 1 trade and quote data for financial options contracts, the associated reference data and the corresponding equity level 1 trades and quotes for the same time period. All data has been sourced from tickdata.com.

The sample dataset has a maximum of approximately 200 million rows for a single date and includes data for 10 underlying securities. The full universe that our clients load is typically much larger, covering thousands of underlying securities. For some of these securities, for example AAPL, the ratio of the number of option quotes to underlying quotes can be in excess of 60:1 on some dates.

It is thus inevitable that when storing equity options data for a large universe of underlying securities, the number of rows per partition will regularly exceed 2 billion. When kdb+ 3.0 was released in 2011 it removed the limit to the number of rows that can be stored in a single partition. This gives us two options for storing massive tables, either storing each day of data in a single partition, or storing each day of data in multiple partitions.

In this paper we cover the use of a multi partitioned database, as whilst kdb+ 3.0 allows the very straight forward option of having a single partition for each date, there are still potential advantages to the approach of storing data across multiple partitions for a single date.

Firstly, when saving data, multiple partitions can be written concurrently, potentially reducing the time required to load data from flat files or persist it from memory. Secondly, when running queries against the database, data from multiple partitions can be read in parallel using secondary threads. In the same way as queries on a database with a single partition per date can read data for multiple days in parallel, now data for the same date can be read in parallel. A third advantage related to database maintenance is that since the size of the individual column data files is reduced, the memory required to apply a sort to the data on disk will be reduced.

Kdb+ provides a simple method to store the data in multiple partitions

for each date by using the par.txt file. When attempting to read data

from a database like this a large number of queries will behave

exactly as they would in a database with only one partition per date.

However there are some cases in which it’s necessary to rework things

a little, most notably in the case of as-of joins. This is covered

below.

Options schema¶

Sorting and indexing the options data is straightforward. If we have the data sorted by underlying security, option contract and finally timestamp we can apply the parted attribute to both underlying security and option contract, allowing us to filter quickly on either column.

More interesting is the way in which we choose to store the underlying security market data so that we can link it to the options data efficiently. The simplest way of accomplishing this would be to store the prevailing value of each underlying alongside the option trades and quote data. These extra columns would either be provided in the source data (as was the case in our sample dataset) or could be pre-calculated with an as-of join and then stored.

The advantage of this method is that we do not need to store any additional underlying market data and there is no overhead when performing lookups to find the prevailing underlying quote or last trade for an option quote or trade. However there are two obvious downsides to using this approach.

The first is that it does not offer any flexibility with regard to how the market data for an underlying security maps to the corresponding option data, e.g. if we wanted to do a window join to look at multiple underlying quotes surrounding each option quote. The second is that a significant amount of extra storage space will be required when the data is de-normalized in this way compared to storing the underlying market data in separate tables and doing joins on demand. Even with a frugal schema for the underlying data, this might add 40-50 bytes of storage for each record (depending on whether condition code and exchange fields can be stored as single characters or symbols are required for example). Given that there will be billions of option quotes per day, this can add hundreds of gigabytes to the daily storage requirements. It is worth noting that this may not be as large a problem as it first appears given the possibilities for data compression.

A second possibility is to store underlying market data as completely separate tables and do any joins we require between the two datasets on a purely ad-hoc basis. This option offers the lightest storage requirements and also gives us full flexibility in how we do the joins. It does, however, come with the cost of extra processing time when searching for the underlying market data related to the option data at query time. Examples of how this is done can be found in the queries section below.

A third option, a combination of the first two, would be to save the option and underlying data as separate tables, but to compute row indices in the underlying market data tables and store them in the option tables as link columns. This requires less space (a single integer column per link to each underlying table) than storing full underlying trade/quote information along with each option table row, avoids having to find the correct underlying trade/quote at query time and also gives flexibility by having all the underlying data available for ad-hoc joins.

Using the third option requires us to ensure that the underlying and option data for the same securities always reside in the same partition. We can achieve this as part of the load process outlined below.

Loading and saving data¶

Here we assume some familiarity with loading large data files by

splitting the file and loading in chunks using .Q.fs and .Q.fsn.

Striping data over multiple partitions per date¶

Firstly we demonstrate how to save a chunk of loaded and parsed data into a database with multiple partitions per date. In our case we will split the data alphabetically by underlying symbol into groups as follows: ABC, DEF, GHI, JKL, MNO, PQR, STU and VWXYZ

We should have a par.txt file containing paths to directories for each

of these symbol groups. The contents of our par.txt file are thus as

follows:

/data/0

/data/1

/data/2

/data/3

/data/4

/data/5

/data/6

/data/7Before demonstrating how we can stripe the data over these

directories, it is worth noting that if future data volumes increase

and we wish to partition the data into a greater number of stripes, we

can do this by adding new directories to par.txt without the need to

go back and repartition old data. We would only need to create empty

tables for each existing date for each partitioned table in our db.

With regard to saving a chunk of data, there are many ways to do this

but we provide an example below where we read in a list of available

partitions and create some helper functions to allow us to easily

partition and save the data. In the code below the directory is

assumed to be a global variable (DIR) giving the path to our par.txt

file in q format (symbol with a leading colon).

// A dictionary mapping alphabetical group to the directory

// in the database we wish to save to

dirs:`ABC`DEF`GHI`JKL`MNO`PQR`STU`VWXYZ!hsym each`$read0 ` sv DIR,`par.txt

// A function which will return a list of partitions

// to which each of a list of symbols should be saved.

getpart:.Q.fu {[symlist]

key[dirs]0 3 6 9 12 15 18 21 bin .Q.A?first each string symlist,()}

saveonepart:{[dt;tablename;data;part2save]

(` sv dirs[part2save],(`$string dt),tablename,`)set

.Q.en[DIR]

delete part from select from data where part=part2save}We could use the following snippet to save some quote data stored in a

variable CHUNK inside a function called by .Q.fs or .Q.fsn. DATE is

assumed to be a global variable here representing the date for which

we are loading data. It is elementary to modify this to include the

possibility of data for more than one date in a particular file load.

This is excluded here for the sake of simplicity.

{

…

CHUNK:update part:getpart underlyingSym from CHUNK;

saveonepart[DATE;`QUOTE;CHUNK]each distinct exec part from CHUNK;

…

}By implementing the previously-defined getpart function to generate

the partition to save down to based on either the underlyingSym column

for options data or the sym column for underlying market data, we can

be sure that related options and underlying data will be stored in the

same partitions.

Once the data has been loaded and saved we will often need to apply an

attribute to one or more of the columns of the data. This is a fairly

easy step as we just need to apply the attribute to a table spread

over multiple directories instead of one. In our example of option

quotes we would like to apply the partitioned attribute (`p#) to

both the sym and underlyingSym columns. We can do this as follows:

// function applies p# attribute to sym and underlyingSym columns

// of the quote table for the specified date and directory

addphashes:{[dt;dir]

{[dt;dir;f]@[` sv dir,(`$string dt),`QUOTE;f;`p#]}[dt;dir]

each `sym`underlyingSym} This may be called after loading all the data in our script:

addphashes[DATE]each value dirs;Adding links to market data¶

If we wish to store links to the underlying data within the option

data, a sensible time to generate and store these links would be just

after we have loaded, sorted and added attributes to the data. We can

do this as part of a loader script with the following code. Here we

just create one link stored in the QUOTE table to the corresponding

quote in the EQUOTE (underlying quote) table:

dirs: `$read0 ` sv DIR,`par.txt

addlinks:{[dt;dir]

dir:` sv dir,`$string dt;

// compute links as an as-of join.

inds:select ind: x from

aj[`sym`timestamp;

select sym:underlyingSym,timestamp from dir`QUOTE;

select sym,timestamp,i from dir`EQUOTE];

// save the links

(` sv dir,`QUOTE`underlying)set `EQUOTE!exec ind from inds;

// update the metadata of the QUOTE table

u set distinct get[u:` sv dir,`QUOTE`.d],`underlying}Again we should use this for each partition for the date we have just loaded.

addlinks[DATE]each value dirs;Example queries¶

In all of the examples below variables in caps are used instead of specific values.

Raw options quote data retrieval with underlying quote¶

In the simplest case where we have the prevailing underlying quote

stored alongside the option quote as columns lastbidPrice and

lastaskPrice our query is:

select sym, timestamp, bidPrice, askPrice, lastBidPrice, lastAskPrice from QUOTE

where date=DATE, sym=SYM, time within (STARTTIME;ENDTIME)For the dataset where we have links to the prevailing underlying quote stored we can use:

select sym, timestamp, bidPrice, askPrice, underlying.bid, underlying.ask from QUOTE

where date=DATE, sym=SYM, time within (STARTTIME;ENDTIME)In the case where we have the options data and underlying data stored in separate tables, we could usually use an as-of join. However, since our database has multiple partitions per date, specifying the right-most argument of the as-of join in the usual way does not behave in the same manner as in the case of databases with a single partition per date. For example, if we look at a standard query to get the prevailing quote as of each trade we encounter some problems.

aj[`sym`time;

select price from TRADE where date=SOMEDATE, sym in SYMLIST;

select sym, time, bid, ask from quote where date=SOMEDATE]In the case of a database with a single partition per date, this as-of join does not read the entire sym, time, bid and ask columns into memory before performing the lookup, rather it searches for the correct rows from a memory map of the quote table. In a database with multiple partitions per date, the following part of the previous query proves problematic:

select sym, time, bid, ask from EQUOTE where date=SOMEDATEThis now causes all of the data to be mapped and read into memory so

that the as-of join can be performed. Not only is this undesirable due

to the extra I/O required but because multiple memory-mapped

partitions are being collapsed into one in memory table, it also has

the detrimental side effect of removing the partitioned attribute

normally found on the sym column since rows with the same symbol could

occur in multiple partitions. This is not something that should

actually occur in this database but since it is possible, kdb+ will

defensively remove the partitioned attribute. In addition, because

part of the reason we chose a database with multiple partitions for

each date was to ensure no single partition was bigger than 2 billion

rows, we may even hit a limit error when trying to do as-of joins

against large tables. (This could only occur when using a version of

kdb+ older than 3.0).

The result of the above is that not only would a join take longer because more data is being read from the disk but also the join itself will be performed much more slowly. A particular technique to work around this would be to create our own function which will perform joins against each memory-mapped partition for a certain date without reading the full table into memory, then aggregate the results from each partition.

In the function below the parameters are specified as follows:

| parameter | denotes |

|---|---|

| c | A list of column names upon which to perform the as-of join, just as we would have with a regular aj |

| t1 | The first table, just as in the case of a regular aj |

| t2 | The second table name, a symbol giving the name of a partitioned table. (To do an as-of join on a non-partitioned table, use a regular aj.) |

| t2d | The date upon which to do the join. (Do one date at a time if there are multiple dates.) |

| t2c | A list of column expressions for the selection from the partitioned table, e.g. (`Ticker;`Timestamp;`Trade;`TradeSize;(log;`TradeSize)) – usually some subset of the column names in the table |

| t2cn | A list of column aliases in the partitioned table e.g. `Ticker`Timestamp`price`size`lnprice |

ajparted:{[c;t1;t2n;t2d;t2c;t2cn]

if[not all c in t2cn;'`missingcols];

/ we want just one row per row in the input, so put a row id as a key

/ and just fill values in the input table with

/ rows that are found for the second table

/ build table a table with the right schema to start

t1:`rid xkey update rid:`s#i from

aj[c;t1;?[t2n;enlist(<;`date;first date);0b;t2cn!t2c]];

/ do aj's on each partition of the second table with the first table,

/ only return rows that we have values for,

/ then upsert these to the keyed t1

delete rid from 0!t1,/

{[c;t1;t2n;t2d;t2c;t2cn;x]

inds@:vinds:where not null inds:

(c#M:?[(` sv`$string x,t2d)t2n;();0b;t2cn!t2c])bin (c#value t1);

1!(0!t1)[vinds],'M inds}[c;t1;t2n;t2d;t2c;t2cn]

peach distinct .Q.pd}Returning to our original example query of getting the prevailing

underlying quote information for a particular set of option quotes, we

can use the following call to the ajparted function:

t1: select sym,timestamp,bidPrice,askPrice from QUOTE

where date=SOMEDATE,sym in SYMLIST,timestamp within (STARTTIME:ENDTIME)

ajparted[`underlyingSym`timestamp;t1;`EQUOTE;SOMEDATE;

`sym`timestamp`bid`ask;`underlyingSym`timestamp`bid`ask]Snapshot of option chain¶

This is an example where we have an underlying symbol and want to get a snapshot of the quotes available for all options at a given time.

Firstly, we will need to query the security master table (called mas

in our case) for all option data available on the given date for this

underlying and then find the last quote available for each option at,

or prior to, the given time.

The available option contracts may be queried from a security master

table, mas, using the following:

optsyms:select sym from mas

where date=OURDATE, underlyingSym=OURSYMNow that we have all of the options contracts we require, the question

becomes how to query the QUOTE table to get the available quote for

each option at the given time. One way to do this would be to write a

query to extract the last quote prior to the time in question for each

option:

select last bid, last ask by sym from QUOTE

where date=OURDATE, sym in optsyms, time<=OURTIMEHowever, this is another place where we would normally use an as-of

join since it allows us to efficiently search for the last record

prior to the time in question rather than scan through all of the

records for each symbol to see if the timestamp constraint is

fulfilled. We can use the same function from the previous example to

do an as-of join here. Firstly, we use the cross function to create a

table of symbol and time pairs in order to carry out the as-of join:

rack:optsyms cross ([]timestamp:1#OURTIME)Now we can use ajparted to find the correct rows from the QUOTE

table

ajparted[`sym`timestamp;rack;`QUOTE;OURDATE;

`sym`timestamp`bid`ask;`sym`timestamp`bid`ask]In the previous example we were able to avoid an ad-hoc as-of join provided we had underlying data (or pre-calculated links to it) stored alongside the options quote data. In this case however, we will need to use an as-of join regardless of how the data is stored.

Building a minutely time series of at-the-money option contracts¶

In our final example, we demonstrate the creation of a minutely time series based on the idea of a generic option contract. In this case we choose a condition specifying this contract as the next expiring call contract nearest to at-the-money.

Initially, we create a time series of minutely bars for the underlying

symbol so we can determine which actual option contract we should use

at each point. Given we are working with relatively low-volume trade

data, we do this with a regular grouping and aggregation query. Note

that we could also use ajparted with a rack of symbol and time pairs

as in the above example.

bars:select last price by time.minute from ETRADE

where date=ourdate, sym=OURSYMWe now need to find the particular contracts that are available on our chosen date and the one that is closest to at-the-money at each point in our series.

We can wrap up the logic for choosing a contract into a function with parameters for date, underlying security, contract type (call or put) and price:

closest2atm:{[d;s;t;p]

/ A list of all the nearest expiring contracts on this date

cands:`strike xasc select sym,strike from mas

where date=d, underlyingSym=s, typ=t, expir=(min;expir)fby underlyingSym;

/ A list of all strike prices with midpoints between,

/ we can then use bin to find the contract with a strike price to our prices

searchlist:1_raze{avg[x,y],x}':[cands`strike];

inds:searchlist bin p;

/ Any odd indices in inds mean price is closer to strike above

/ add one to these and divide everything by 2 to give the indices into cands

inds[where 1=inds mod 2]+:1;

inds:inds div 2;

/ return the list of at-the-money symbols

cands[`sym]inds}

update sym:closest2atm[OURDATE;OURSYM;"C";price] from `barsFinally we query the closing bid and ask for each of these bars:

ajparted[

`sym`timestamp;

select sym, minute, timestamp:`timespan$minute, price from bars;

`QUOTE; OURDATE;

`sym`timestamp`bid`ask; `sym`timestamp`bid`ask]Compression¶

The use of compression for all or part of the dataset here is outside the scope of this white paper, however, this is undoubtedly an important feature to consider using for options data.

Knowledge Base: File compression

Conclusion¶

Storing and querying options data can present challenges due to the volume of data involved. While the introduction of kdb+ 3.0 lets clients easily handle the ever-increasing data volumes by removing the per-partition limit of 2 billion rows, there are still several potential benefits to storing the tick data in multiple partitions per date as outlined in Overview of the dataset. As we have seen however, in choosing this approach it will be necessary to write some queries in a different way to achieve the best performance.

Regardless of whether the data is stored in a single partition per date or in a multi-partitioned manner, the choice of schema will still impact the storage space required for the data and queries against the database. Here we have presented several different schema choices and examples of several simple queries implemented for each schema.

Author¶

James Hanna has helped design and develop kdb+ implementations and proof of concepts for more than 40 customers. Based in New York, James is a Technical Architect for KX, a high-performance data-management, event-processing and trading platform.